New York Life Illustration Is Concisely Informative

Posted at Advisors4Advisors.com on March 26, 2011

A few days ago I praised ING’s unusually useful inforce illustration for one of its no-lapse universal life policies. As Insurance Company Appreciation Minute ends, I also want to give high marks to New York Life’s sales illustrations for its Universal Life – Lifetime Guarantee policies. This no-lapse universal life product was replaced by a redesigned product (Custom Universal Life Guarantee) in 2010, and that product’s illustrations are also good.

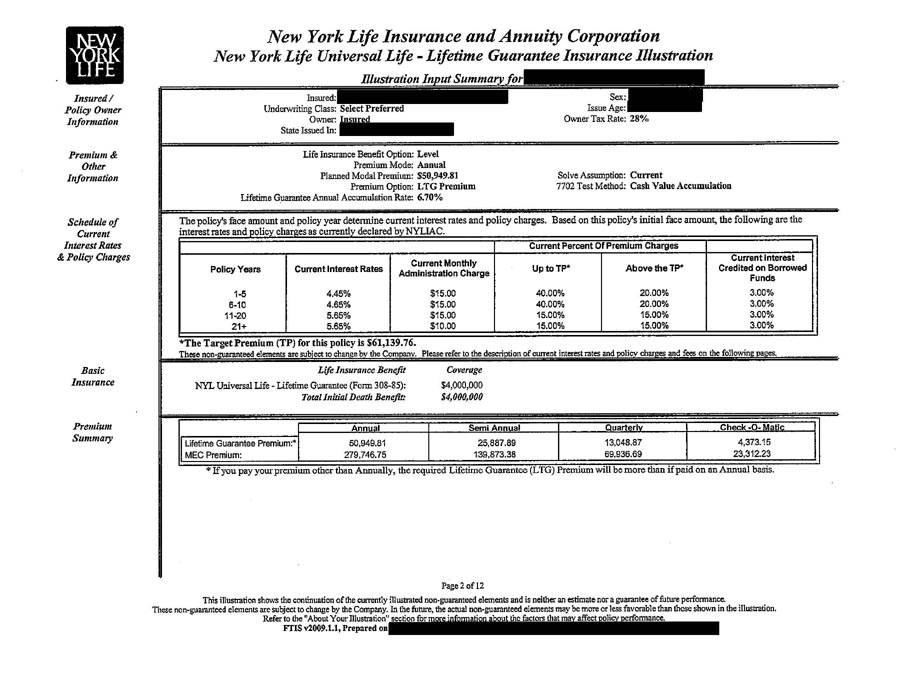

On one page of its Universal Life – Lifetime Guarantee illustrations, New York Life managed to give knowledgeable buyers and their advisors the information needed to choose a premium payment schedule.

Universal Life – Lifetime Guarantee uses a stipulated premium design for the no-lapse guarantee. The policy remains in force as long as the actual premiums paid accumulated at the Lifetime Guarantee Annual Accumulation Rate exceed the Required Lifetime No Lapse Guaranteed Benefit (NLGB) Monthly Premiums accumulated at the same rate. This comparison of compounded amounts is done each month.

The sales illustration discloses the Lifetime Guarantee Annual Accumulation Rate; in this example, it is 6.70%, guaranteed for the life of the policy. The required monthly premium is $4,373.15, shown in the Premium Summary section as the Check-O-Matic mode of the Lifetime Guarantee Premium. The annual Lifetime Guarantee Premium is $50,949.81, and you can verify that this is the present value of 12 premiums of $4,373.15 discounted at the monthly equivalent of 6.70%.

You have to pay at least $4,373.15 each month, but you can pay more if you choose. To decide if it makes sense to prepay future monthly premiums, you need to know what the discount rate is. In this case, it’s 6.70%, after tax. You also need to estimate the probability of death during the prepayment period, because you don’t get a refund of excess payments at death.

Universal Life – Lifetime Guarantee also has nonguaranteed cash surrender values, which tend to be higher than those for other no-lapse universal life policies. The same page of the sales illustration says that during the first 10 years the current percent-of-premium charge is 40% up to a Target Premium of $61,139.76 and 20% above that, and the charge drops to 15% after 10 years.

There is no surrender charge, so the percent-of-premium charge has a big impact on the cash surrender values. New York Life created an incentive to bunch up the premiums; for example, instead of paying $50,949.81 each year, you could pay $101,899.62 in the first year and nothing in the second year. That would reduce the two-year sum of percent-of-premium charges by $8,151.97, because $40,759.86 of the $101,899.62 first-year premium would be subject to only a 20% charge. And that cost saving will increase the cash surrender value.

New York Life also created an incentive to skip premiums in Year 10 and pay more in Year 11, because the premium charge will be 15% rather than 40%.

Most consumers probably do not appreciate how much information is shown on this one page. I don’t know how many advisors appreciate it.